Credit card debt has become a pressing issue for millions of Americans, blending financial data with deeply personal struggles. This article explores the moral questions behind accumulating plastic debt, examines its emotional toll, and offers practical guidance for breaking free from the burden.

The Growing Burden of Credit Card Debt

In early 2026, U.S. credit card debt surpassed $1.17 trillion, with projections edging toward $1.18 trillion by year-end. The average cardholder balance climbed to $6,730, while prime-plus consumers carried an average of $10,700. As of Q2 2025, credit card balances soared by $27 billion, a 6% year-over-year increase. These figures illustrate a pervasive trend: more households rely on revolving credit to cover both emergencies and everyday expenses.

Behind these numbers lies a story of skyrocketing balances and mounting interest that can trap individuals for years. Nearly half of U.S. cardholders carry balances month to month, and 61% have been in debt for over a year. For 31%, the struggle extends beyond three years, and 21% have been battling debt for at least five years. This enduring cycle highlights a challenge that goes beyond simple budgeting—it raises questions about fairness, access, and consumer responsibility.

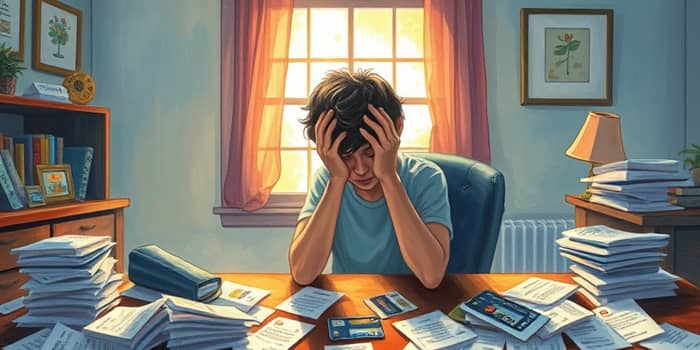

The Emotional Toll and Psychological Impact

Debt often carries invisible weights: daily anxiety, sleepless nights, and a persistent fear that relief might never come. According to a recent survey, 22% of debtors doubt they’ll ever pay off their balances, and 27% feel less confident about escaping debt than they did the year before. For many, the act of making only minimum payments creates a sense of futility, reinforcing the belief that freedom is out of reach.

These emotional realities are compounded by the stigma of financial struggle. People can feel shame discussing credit card balances with friends or family. Yet acknowledging the problem and seeking support can be the first step toward healing. Recognizing that stress and anxiety about debt are widespread can help individuals feel less isolated and more empowered to take action.

Ethical Tensions: Responsibility vs Systemic Pressures

Credit card debt sits at the intersection of personal choices and broader economic forces. On one hand, consumers are encouraged to spend by marketing and rewards programs. On the other, interest rates often exceed 20%, creating what critics call a minimum payment trap that deepens crisis and enriches card issuers.

- Predatory lending tactics target vulnerable consumers with high APRs.

- Reward programs incentivize spending that may exceed budgets.

- Economic inequality amplifies the burden for lower-income households.

Debtors must weigh personal accountability against systemic factors such as rising living costs, healthcare expenses, and limited wage growth. When 41% of card balances originate from unexpected financial emergencies and repairs, compassion and policy reform become as crucial as individual discipline.

Navigating the Minimum Payment Trap

Making only the minimum payment may seem like a manageable option, but it’s a financial quagmire. Consumers can spend decades chipping away at balances that continue to accrue high interest. To illustrate, consider the average APR for different card types:

Even a seemingly small balance of $5,000 can cost thousands more in interest if only minimum payments are made. This reality underscores the importance of tackling debt aggressively with a clear plan.

Practical Strategies for Breaking the Cycle

Escaping the debt cycle requires a combination of mindset shifts and actionable steps. Consider these tactics:

- Create a realistic budget that prioritizes debt repayment over discretionary spending.

- Build an emergency fund to avoid pulling out cards for unplanned expenses.

- Explore balance transfer offers or low-interest cards to reduce APR.

- Negotiate with creditors for lower rates or hardship programs.

- Use the debt-snowball or debt-avalanche method to gain momentum and pay off high-interest balances first.

By taking control of spending habits and leveraging available tools, individuals can begin to chip away at their obligations. Small victories—such as reducing one balance or receiving a lower interest rate—can build confidence for the long haul.

A Hopeful Path Forward

Despite the challenges, there is reason for optimism. Federal Reserve rate cuts on the horizon could lower borrowing costs, and projected economic growth may boost wages and job opportunities. With inflation expected to ease and unemployment rising only slightly, consumers could see a cautiously optimistic outlook for relief.

- Federal Reserve cuts may reduce APRs and ease monthly payments.

- Rising wages could improve debt-to-income ratios.

- Growth in credit counseling services provides free guidance.

Ultimately, the journey out of credit card debt is personal and ethical. It demands both self-reflection and external changes—policy reforms, transparent lending practices, and community support. By weaving together practical strategies and a compassionate perspective, individuals can navigate the moral complexities of debt and move toward financial freedom.

Confronting credit card debt is not just a matter of numbers—it’s a test of character and resilience. Each payment made, each budget adjusted, and each resource tapped brings you one step closer to breaking free from the long-term debt cycle of despair. In doing so, you reclaim control, restore hope, and set the stage for a more secure and empowering financial future.

References

- https://www.solosuit.com/posts/credit-card-debt-statistics

- https://use.expensify.com/blog/credit-card-statistics

- https://www.lendingtree.com/credit-cards/study/credit-card-debt-statistics/

- https://newsroom.transunion.com/2026-consumer-credit-forecast/

- https://www.bankrate.com/credit-cards/news/credit-card-debt-report/

- https://www.federalreserve.gov/releases/g19/current/

- https://fred.stlouisfed.org/series/CCLACBW027SBOG

- https://www.youtube.com/watch?v=h2XaSOp_Llk

- https://www.nationaldebtrelief.com/resources/credit-card-debt-relief/credit-card-debt-stats/